You will remain on the same site

This piece talks about a term loan in South Africa that comes with steady payment schedules. It mentions how these loans, provided by banks such as Standard Bank, ABSA, FNB, and Nedbank—and also by licensed non-banks—help you know what you’ll pay each month. Even without collateral, these loans make it clear how much you owe each month.

We simplify things here, detailing term loans in South Africa with set payback terms. These include loans up to R300,000 you can pay over time. You’ll understand the basics, comparisons, and examples to see if this loan type suits your needs.

If you earn a salary, own a small business, or need money for debt, home fixes, school, or big buys, this article is for you. It talks about loans in South Africa and mentions the National Credit Act. This Act helps make sure costs are clear and that you can afford the loan.

Fixed repayment loans are now more sought-after due to changing interest rates. They offer certain monthly payments, making it easier to plan your budget. This article will also cover how these loans work, their benefits, how to get one, and what to consider when borrowing without collateral. Plus, it’ll discuss ways to keep your finances safe.

Key Takeaways

- Term Loan with stable monthly amounts helps borrowers plan and budget more easily.

- Term loan SA options include both bank and licensed non-bank lenders under the National Credit Act.

- A fixed repayment loan fixes your monthly payment, reducing exposure to rate swings.

- Unsecured lending can offer quick access, but check affordability and full cost of credit.

- Borrowers seeking up to R300,000 should compare repayment terms, fees, and early-repayment rules.

Understanding Term Loan basics for predictable payments

A Term Loan is money lent that’s paid back in fixed amounts over time. It’s great for paying off debt, getting a car, fixing up your house, medical bills, or school fees. In South Africa, you can pick between loans that need collateral (secured) and those that don’t (unsecured). Unsecured loans don’t need collateral but usually have higher interest rates than secured ones.

Term Loan

What is a Term Loan and how it works

When you get a Term Loan, you receive all the money at once and agree on a payment plan. Each payment includes interest and part of the money you borrowed. At first, you pay more interest than principal, but over time, you pay off more of the principal. Lenders give you an amortization schedule. It shows payment dates, how each payment is split, and when the loan will be fully paid off.

Key features that create predictable payments

Predictable payments are possible through fixed interest rates or amounts. The loan agreement will show all fees and the annual rate (APR), as the law requires. Many people set up automatic payments and use online accounts to stay on track. Knowing all the fees and having an amortization schedule helps families manage their budgets better.

Difference between fixed repayment loan and variable-rate loans

Fixed repayment loans keep your payments the same, making budgeting easier. Variable-rate loans tie your interest to market rates, so your payments can change over time. In South Africa, the Reserve Bank’s prime rate affects variable loans.

Fixed loans are more predictable but might start with higher rates. Variable loans could be cheaper at first but might increase later. Choosing one depends on whether you prefer steady payments or can handle changing rates when managing your money.

Benefits of fixed repayment loan for borrowers in South Africa

A fixed repayment loan offers clear, predictable payments. This helps households plan their budgets and handle monthly expenses without any sudden changes. Lenders offering term loans in SA share APR and repayment details beforehand. This way, applicants know if they can afford the loan before they agree to it.

Budgeting advantages with stable monthly installments

Fixed monthly payments make managing money easier. Knowing your exact payment each month lets you plan for rent, food, and bills without needing to borrow money last minute.

For those earning a steady income, such predictability is a relief. It lowers stress by reducing the risk of missing a payment when interest rates change.

How long term instalments reduce financial strain

Longer repayment periods make monthly payments smaller. Lenders might offer terms from 24 to 72 months, based on the loan size and type.

With lower payments each month, you can afford big expenses without using your savings or credit cards. However, you’ll face interest for a longer time and pay more in the end.

Comparing total cost of credit: fixed vs. fluctuating rates

To compare loans, multiply the monthly payment by the total months. A fixed loan keeps payments the same, making its total cost clear from the start.

Loans with variable rates might start off cheaper, but they can increase with market rates. This adds uncertainty. By comparing APR and effective annual rate, borrowers can properly compare different lenders.

- Use fixed rates for big purchases or when you need certain payments.

- Opt for long-term payments if you need smaller monthly amounts.

- Look at the total interest before deciding on a Term Loan.

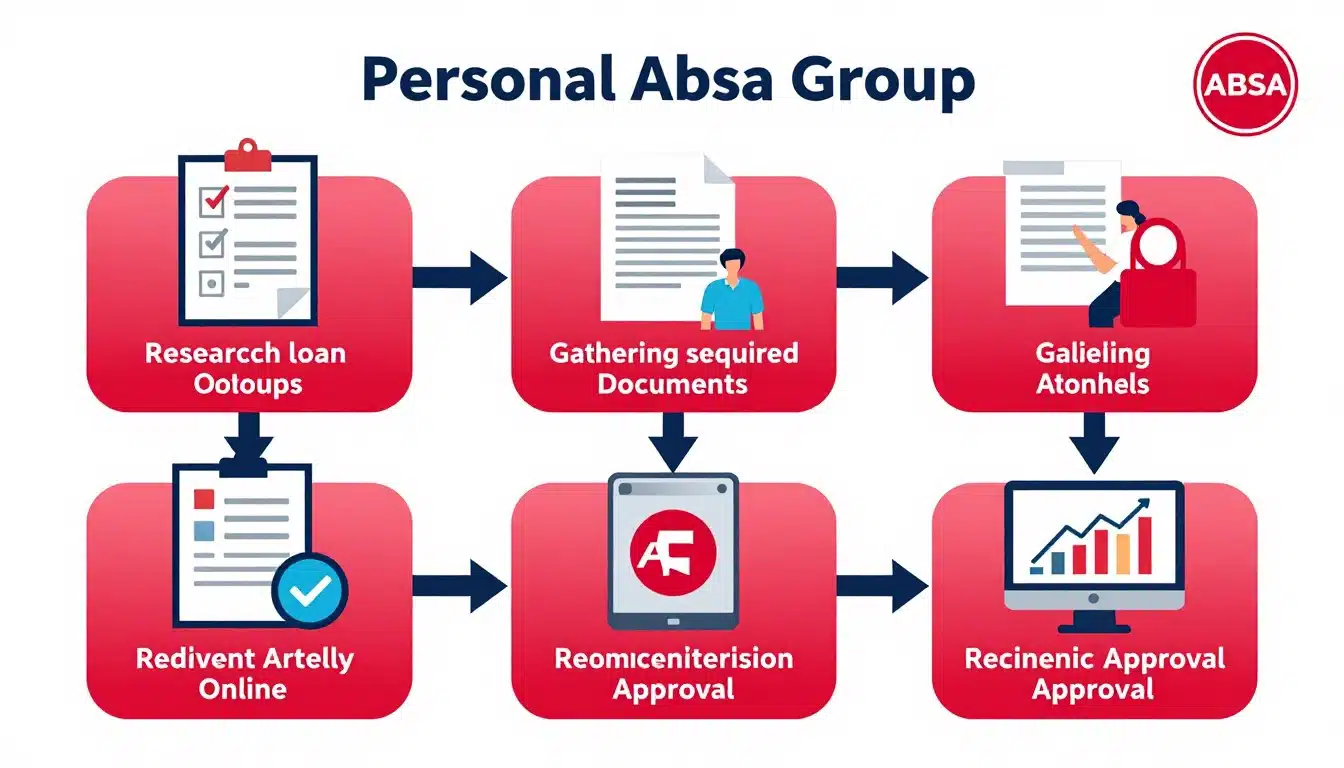

Eligibility and application process for term loan SA

Before applying for a term loan SA, know what’s needed. Lenders need proof of who you are, that you have steady income, and that you can pay back the loan within your budget. This guide will show you what to get ready for a loan without security and explain how applying works.

Basic eligibility criteria for unsecured lending

- You need to be a South African citizen or have permanent residency, usually 18 years old or more.

- There’s a minimum monthly income the lender requires, along with proof of regular work or being self-employed.

- Your spending compared to your income is checked to see if you can afford the loan, as per the National Credit Act.

- Even if your credit isn’t perfect, some lenders might still give you a loan but with possibly higher costs or shorter loan duration.

Required documents and credit checks

- A valid South African ID or passport, and something like a bill to show where you live.

- You’ll need bank statements from the last 3–6 months and payslips or other income proof.

- Employers might need to confirm your job if the lender asks.

- Lenders check your credit through companies like TransUnion, Experian, or Compuscan to find any debt issues or legal judgments.

- They also do checks to confirm your identity and to prevent money laundering, which is standard.

Step-by-step application timeline and approval expectations

- First, pick how much money you want and for how long, then fill out a form online or at a branch.

- A soft credit pull is usually done first to estimate rates without hurting your credit score.

- For the full application, submit all documents so the lender can do a thorough credit check and confirm your earnings.

- Once approved, the lender gives you a loan contract with a set payment schedule to agree to.

- After you sign and meet any last requirements, the money is given to you. This can happen within a day or three for online loans, and even quicker at big banks.

For loans up to R300,000 without security, the process is typically simple. But, for larger amounts, the checks may be stricter. Keep all your documents organized to make approval quicker and smoother.

Borrow up to R300000: loan amounts, terms, and repayment plans

In South Africa, many people borrow up to R300000 with a Term Loan for big spends. They avoid using savings this way. Different term lengths and repayment plans are there to match monthly costs and total interest. Looking at different options makes it easier to see the best choice.

Typical term lengths and installment schedules

Loans up to R300,000 can last from 12 to 72 months. They fit well for people with regular jobs. For contractors and people working gigs, there are paying options every week or two.

For example, a R100,000 loan paid over 36 months means higher monthly payments than over 60 months. The shorter plan saves on total interest but costs more each month. The longer plan is cheaper each month but ends up costing more in interest.

How loan amount affects monthly payment and interest

When you borrow more, monthly payments go up if the rate and time don’t change. Bigger loans also mean paying more interest in total. Lenders look at your income and credit history before saying yes to big unsecured loans.

With amortization, early payments focus on interest more than the principal. But as you pay off the principal, interest becomes a smaller part of your payments. This shift lets you lower the balance faster towards the end.

Early repayment, penalties, and refinancing options

The National Credit Act lets people pay off their loans early following certain rules. Many lenders agree to let you pay early, in full or in part. Partial early payments might reduce the term or monthly payments, depending on what the lender decides.

Some charge fees or give back some interest if you settle the loan early. Always ask for a detailed cost breakdown and the terms for early payment before you agree. Refinancing—combining several payments into one—can make monthly payments lower. However, if it stretches the loan term, you might pay more interest overall.

Risks and considerations for unsecured lending and long term instalments

Choosing a Term Loan or fixed repayment loan has trade-offs. Unsecured loans are quick to get without collateral but have higher interest and fees. Long term instalments make payments easier each month, but you’ll pay more over time. Always read the terms carefully and check if you can really afford the loan before you sign.

Understanding interest rate implications and affordability

Make a budget that includes loan payments, rent, groceries, and transport. Also plan for unexpected costs. Test your budget against possible income drops to ensure you can keep paying over the long term.

Loans with fixed repayments help with monthly budgeting. But, they don’t protect you from unexpected expenses like medical bills. Unsecured loans might have higher rates compared to secured loans. Always include fees and insurance when figuring out the total cost.

Consequences of missed payments and default

If you miss payments, you could face late fees and more interest. Failing to pay can lead to collection efforts and damage your credit score. This makes borrowing harder and more expensive in the future.

A bad credit history affects future loan opportunities. In South Africa, lenders follow the National Credit Act for debt collection. You can talk to them about changing your repayment plan if needed.

Mitigation strategies: insurance, emergency funds, and repayment pauses

Getting insurance like payment-protection can help cover loan payments if you can’t work. Check the policy details to make sure it’s a good deal.

Have an emergency fund that can cover 3 to 6 months of expenses. This helps prevent loan defaults during tough times.

Talk to your lender early if you need help with payments. They might offer payment breaks or loan restructuring. These options can help in the short term, even though they might increase what you pay in interest. Being proactive is key to finding solutions.

Conclusion

Getting a term loan with set payments helps you plan your budget better. In South Africa, you have choices between banks and licensed non-bank lenders for term loan SA options. These loans can be tailored to fixed repayment plans or unsecured lending. You can borrow as much as R300000. This helps spread costs over time, easing cash flow issues and reducing immediate financial stress.

It’s important to look at the total cost before you sign anything. This means comparing APR, origination fees, and any penalties for paying off early or refinancing. Make sure you’re clear on the eligibility requirements and what documents you’ll need. This helps you understand your chances of getting approved. For those who prefer fixed repayment loans, it’s crucial to confirm if the interest rate stays the same throughout the loan term and what the penalties for early repayment or refinancing are.

Start by looking at offers from well-known South African banks like Standard Bank, ABSA, FNB, and Nedbank. But don’t forget about licensed non-bank lenders too. Always ask for a full cost breakdown and go through the loan agreement thoroughly. Consider using safeguards like loan insurance or having an emergency fund to minimize risk. Additionally, checking rates through a soft pre-qualification might be wise, as it doesn’t hurt your credit score.

If you’re finding the decision difficult, talking to a certified financial planner or an accredited debt counsellor can help. They should be familiar with South African laws. A quick review by a pro can help you decide if an unsecured or a secured loan is the best way to borrow up to R300000. This can also ensure you keep your financial health steady in the long run.

Conteúdo criado com auxílio de Inteligência Artificial